Pay Off Debt Faster. Starting Today.

How I went from bankruptcy to over $1M net worth.

How I went from bankruptcy to over $1M net worth.

In under an hour you will learn the exact 4-step system I built after bankruptcy. I went from nothing to over $1M net worth.

Get your exact debt-free date in under 5 minutes

and see how much interest you could save by paying your cards in the best order.

Plug in your balances + rates + minimums and get a clear payoff roadmap plus your debt-free date so you can finally feel in control again.

*screenshots of my personal portfolio.

Because the other side of debt can look like this.

You don’t need

To ghost your friends because you "can't afford" to go out anymore

A side hustle or second job (you're already tired enough)

Perfect credit to start (we're rebuilding that toxic mess too)

A finance degree to decode what the banks are actually doing to you

here's what you dO need

The Breakup Plan.

The exit strategy. The "I'm done being drained" roadmap.

This isn't about punishing yourself. It's about getting relief. You'll learn how to make your current income work smarter, negotiate better rates (because debt doesn't get to call ALL the shots), and let automation handle the heavy lifting while you live your life.

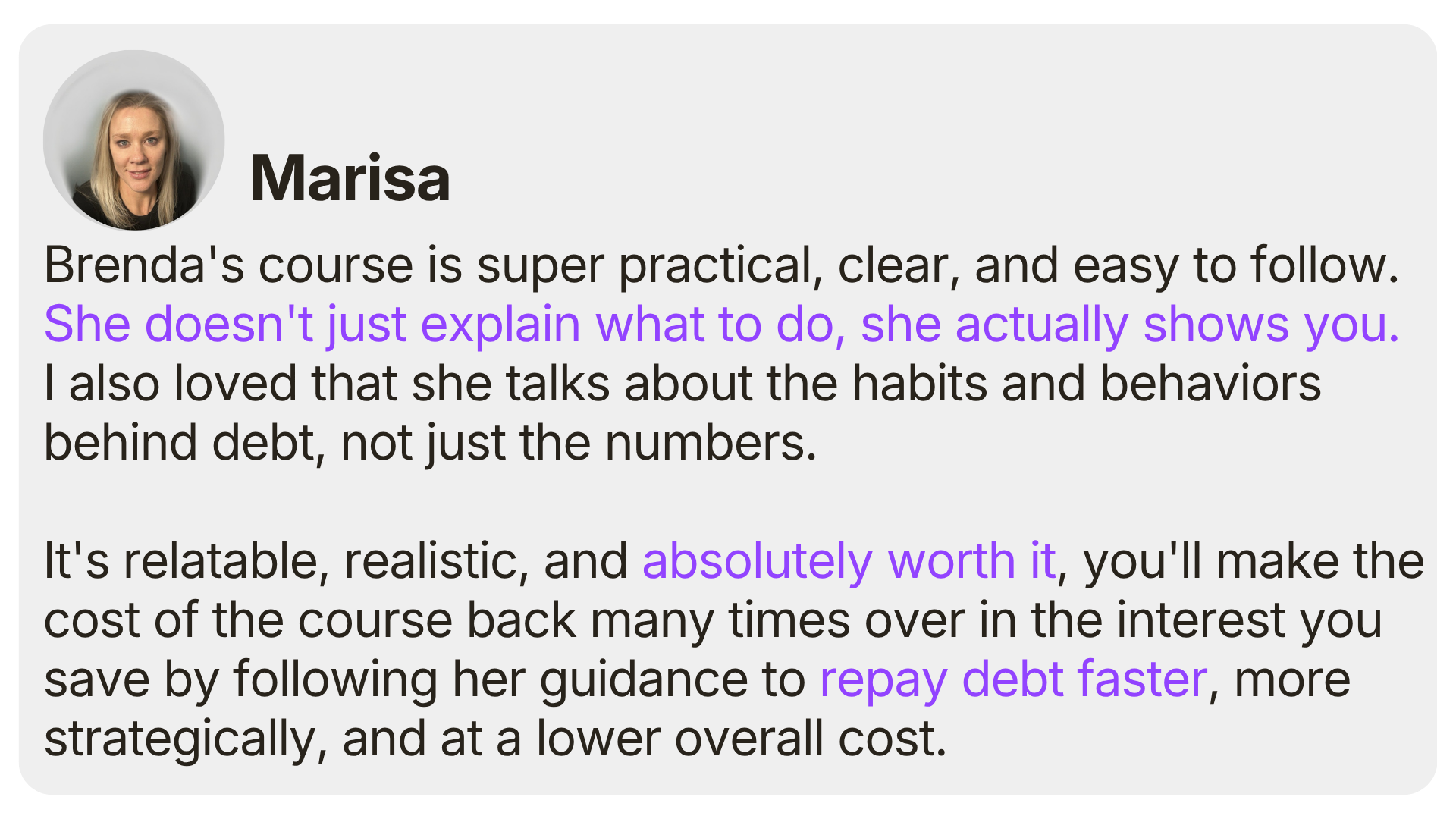

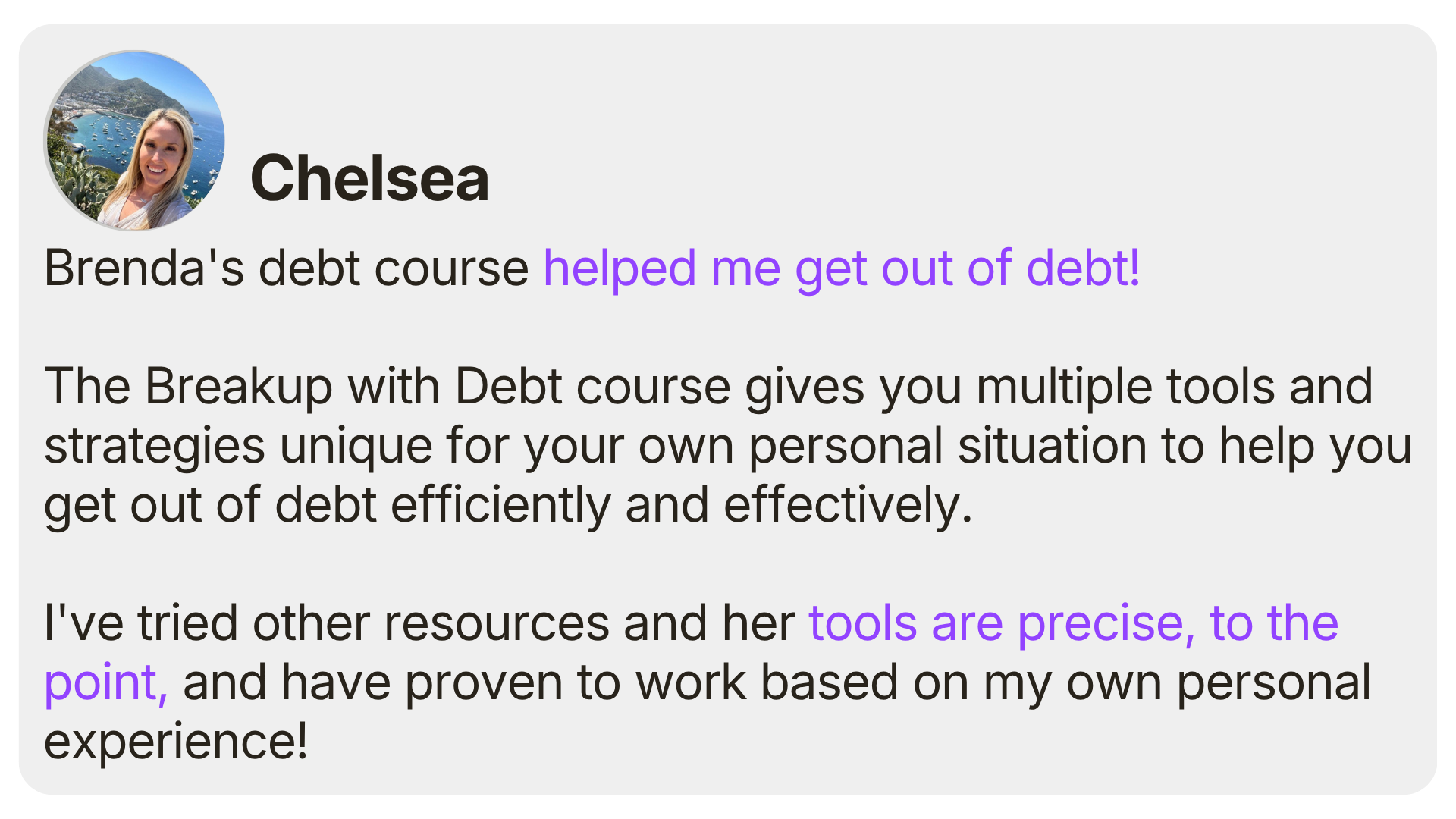

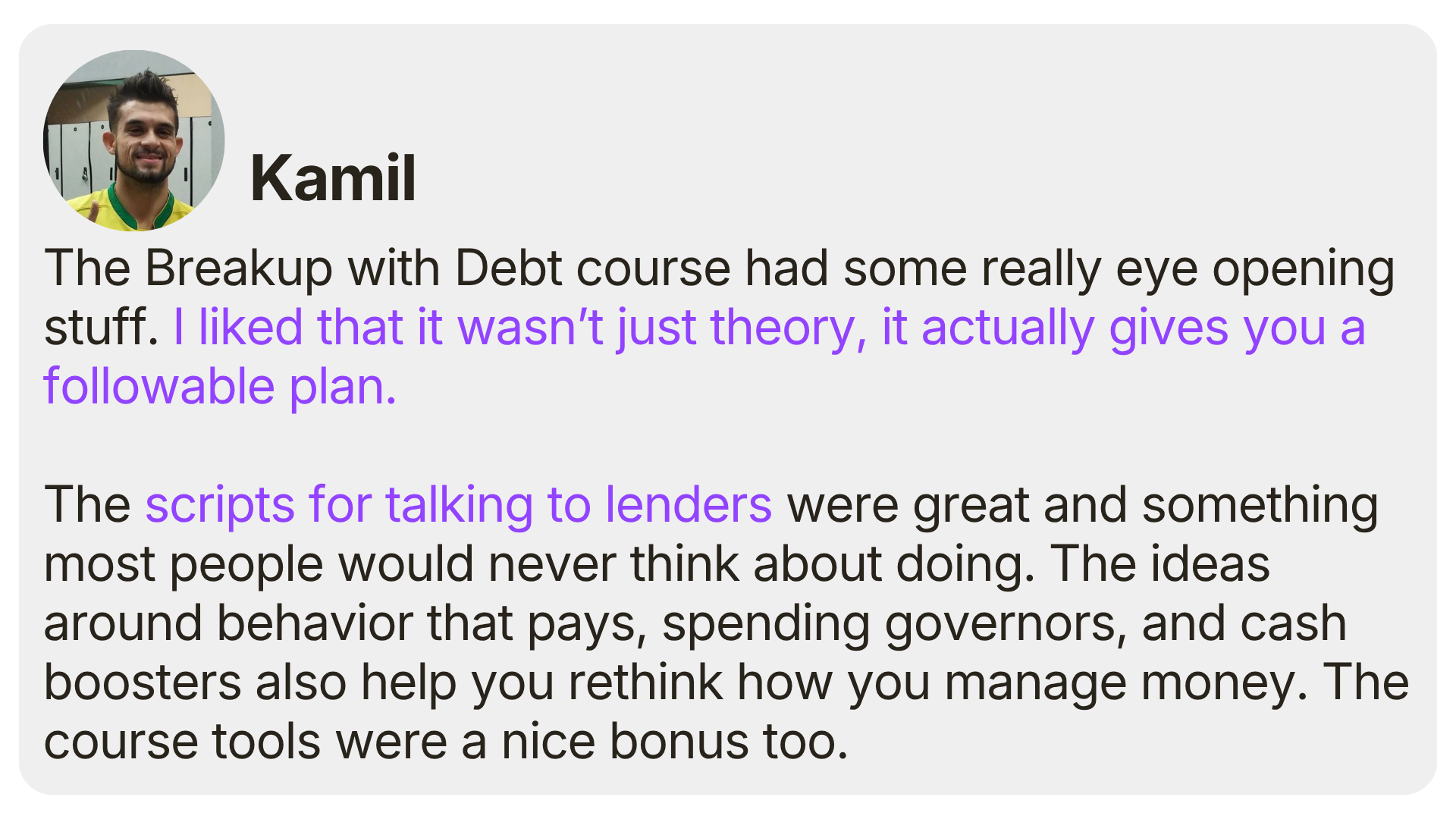

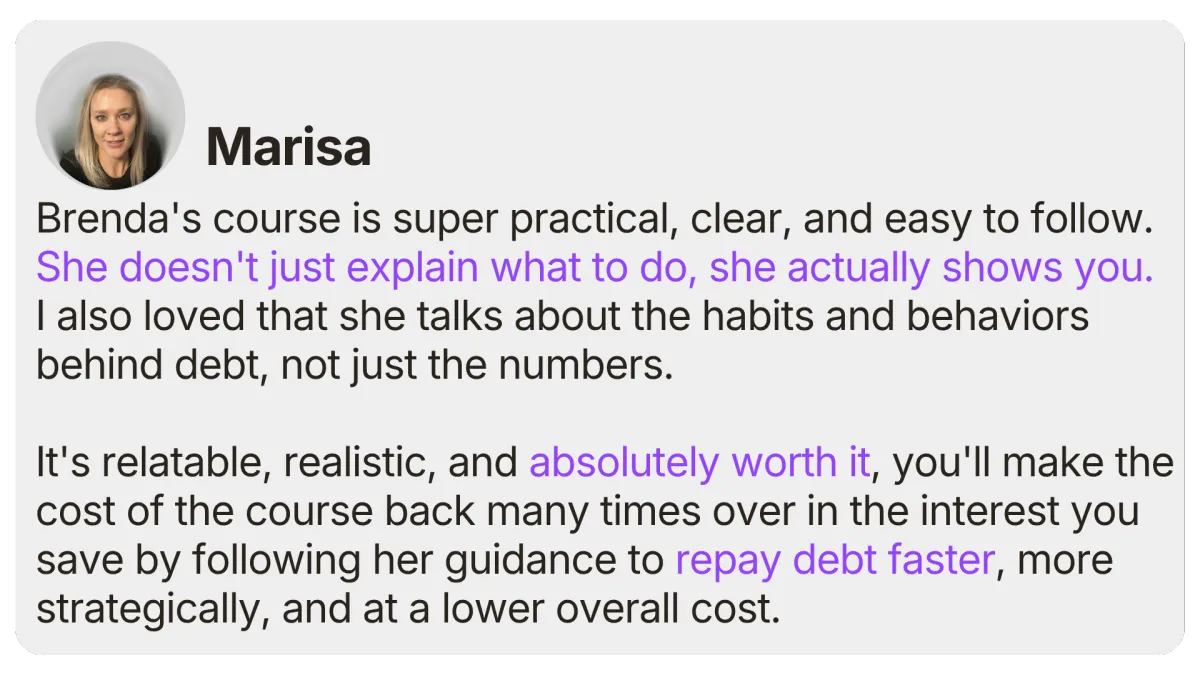

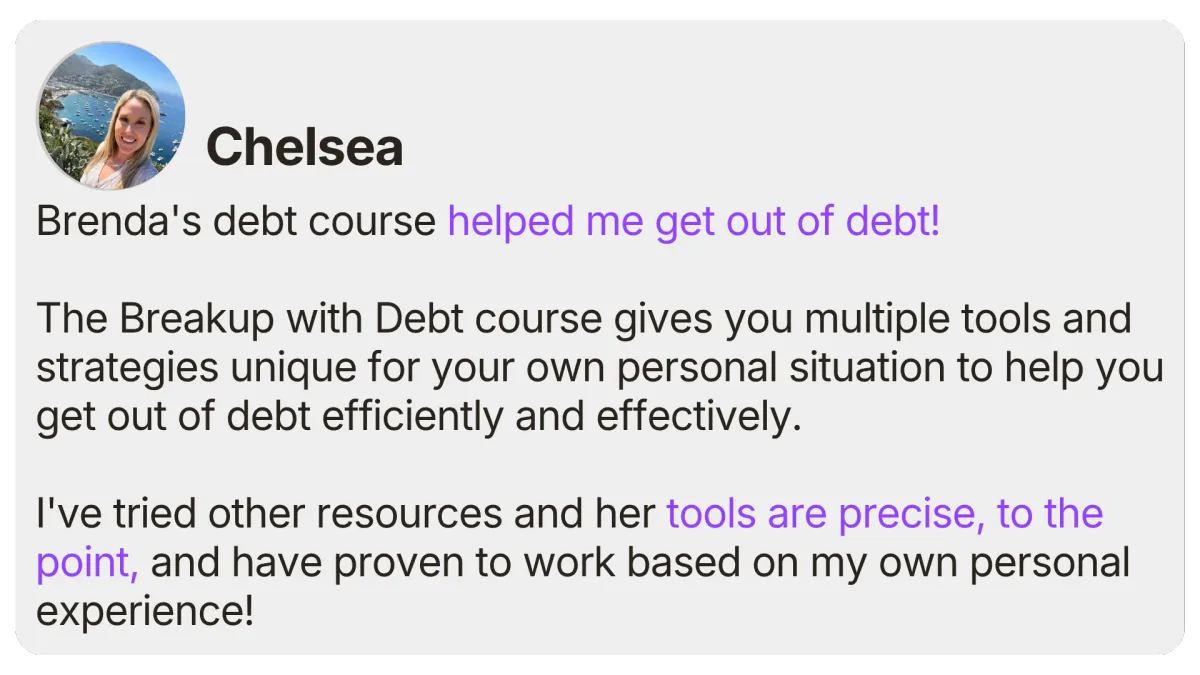

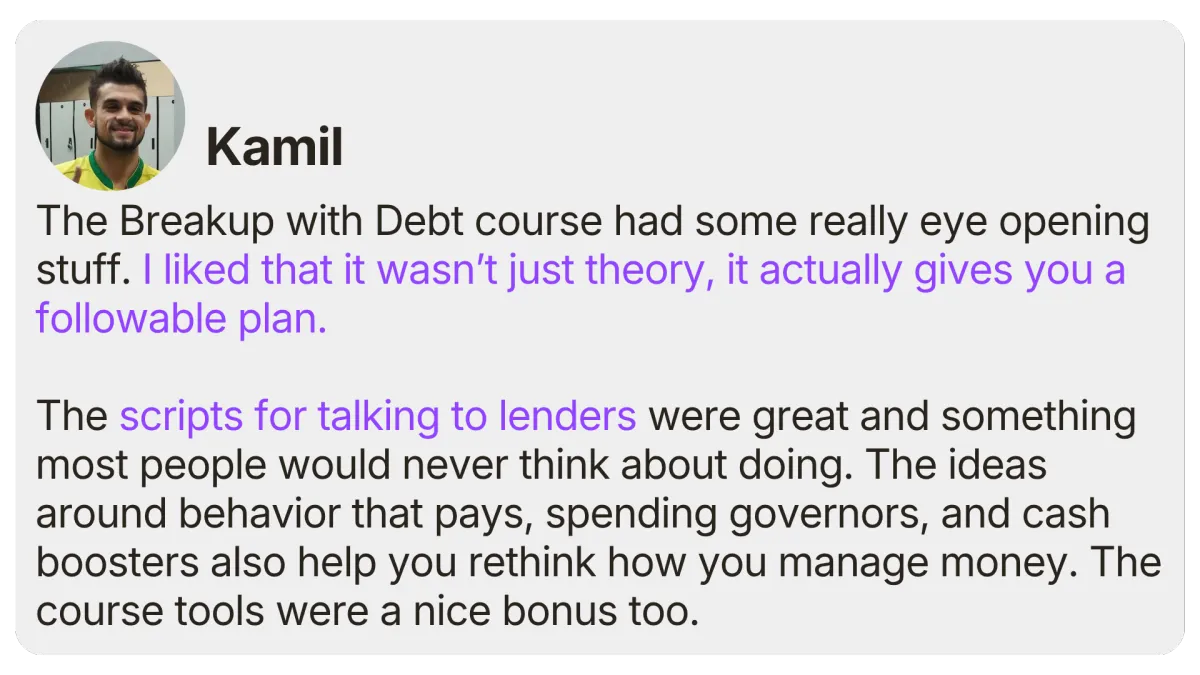

Success stories

Here's what students are saying...

Success stories

Here's what students are saying...

what's included?

5 Complete Training Sections

20+ videos walking you through the breakup, step by step)

The 2 Proven Debt Payoff Strategies:

Choose Avalanche or Snowball and know exactly which debt to attack first.

The Balance Transfer & Personal Loan Playbook

When and how to use these tools to slash your interest rates

The "Set It and Forget It" Automation System

Set up autopay, optimize statement dates, and let payments happen automatically

5 Credit Score Levers You Can Pull Right Now

Boost your score fast, including the trick that adds 40+ points in 30 days

whats included?

5 Complete Training Sections

20+ videos walking you through the breakup, step by step)

The 2 Proven Debt Payoff Strategies:

Choose Avalanche or Snowball and know exactly which debt to attack first.

The Balance Transfer & Personal Loan Playbook

When and how to use these tools to slash your interest rates

The "Set It and Forget It" Automation System

Set up autopay, optimize statement dates, and let payments happen automatically

5 Credit Score Levers You Can Pull Right Now

Boost your score fast, including the trick that adds 40+ points in 30 days

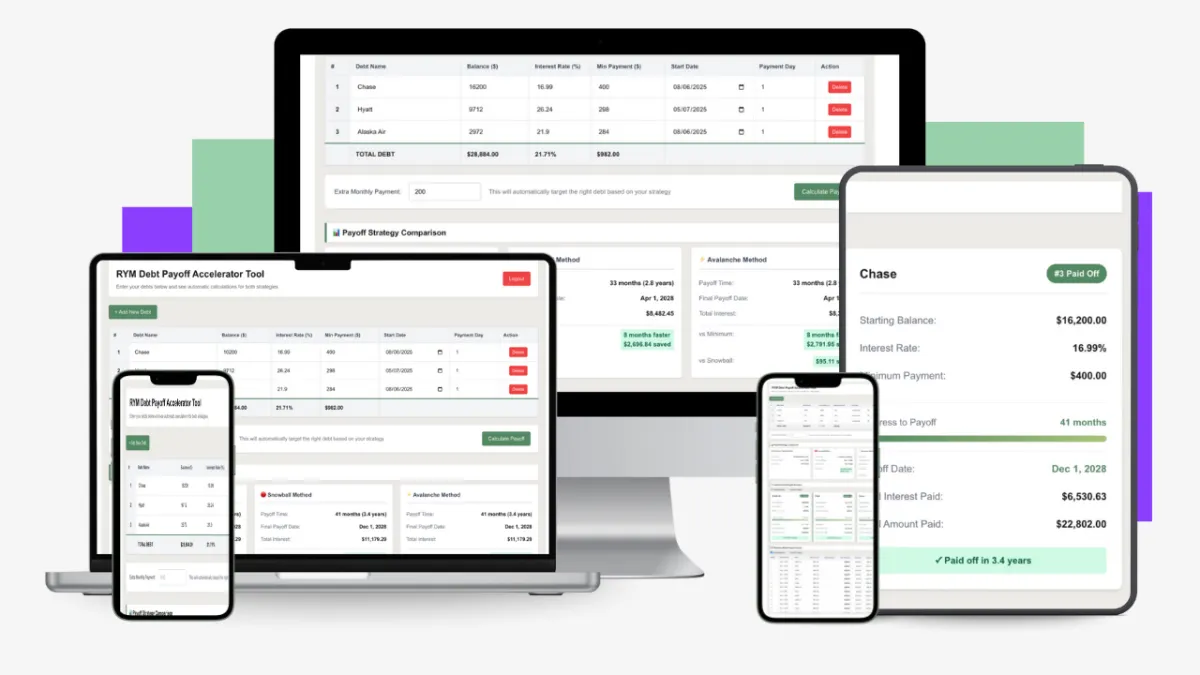

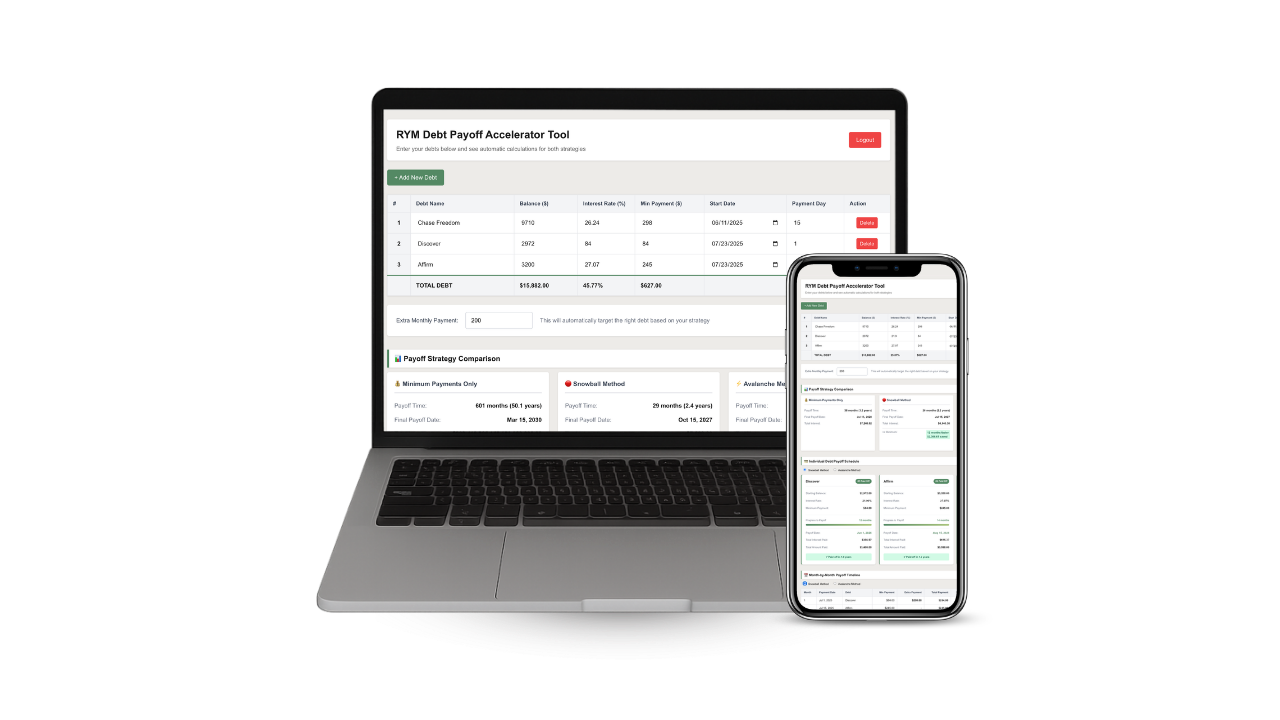

free bonus: Debt Payoff Accelerator

Pay Off Debt Faster.

Starting Today.

In under an hour you will learn the exact

4-step system I built after bankruptcy. I went from nothing to over $1M net worth.

Because the other side

of debt can look like this.

*screenshots of my personal portfolio.

you don't need

To ghost your friends because you "can't afford" to go out anymore

A side hustle or second job (you're already tired enough)

Perfect credit to start (we're rebuilding that toxic mess too)

A finance degree to decode what the banks are actually doing to you

Here's what you do need

The Breakup Plan. The exit strategy.

The "I'm done being drained" roadmap.

This isn't about punishing yourself. It's about getting relief. You'll learn how to make your current income work smarter, negotiate better rates (because debt doesn't get to call ALL the shots), and let automation handle the heavy lifting while you live your life.

success stories

what's included?

5 Complete Training Sections

20+ videos walking you through the breakup, step by step)

The 2 Proven Debt Payoff Strategies:

Choose Avalanche or Snowball and know exactly which debt to attack first.

The Balance Transfer & Personal Loan Playbook: When and how to use these tools to slash your interest rates

The "Set It and Forget It" Automation System: Set up autopay, optimize statement dates, and let payments happen automatically

5 Credit Score Levers You Can Pull Right Now: Boost your score fast, including the trick that adds 40+ points in 30 days

free bonus:

Debt Payoff Accelerator

Enter your balance, APR, and minimum payment.

Get a clear payoff plan in seconds, with every extra dollar mapped out so you know exactly what to do next.

$27 Free*

Enter your balance, APR, and minimum payment.

Get a clear payoff plan in seconds, with every extra dollar mapped out so you know exactly what to do next.

$27 Free*

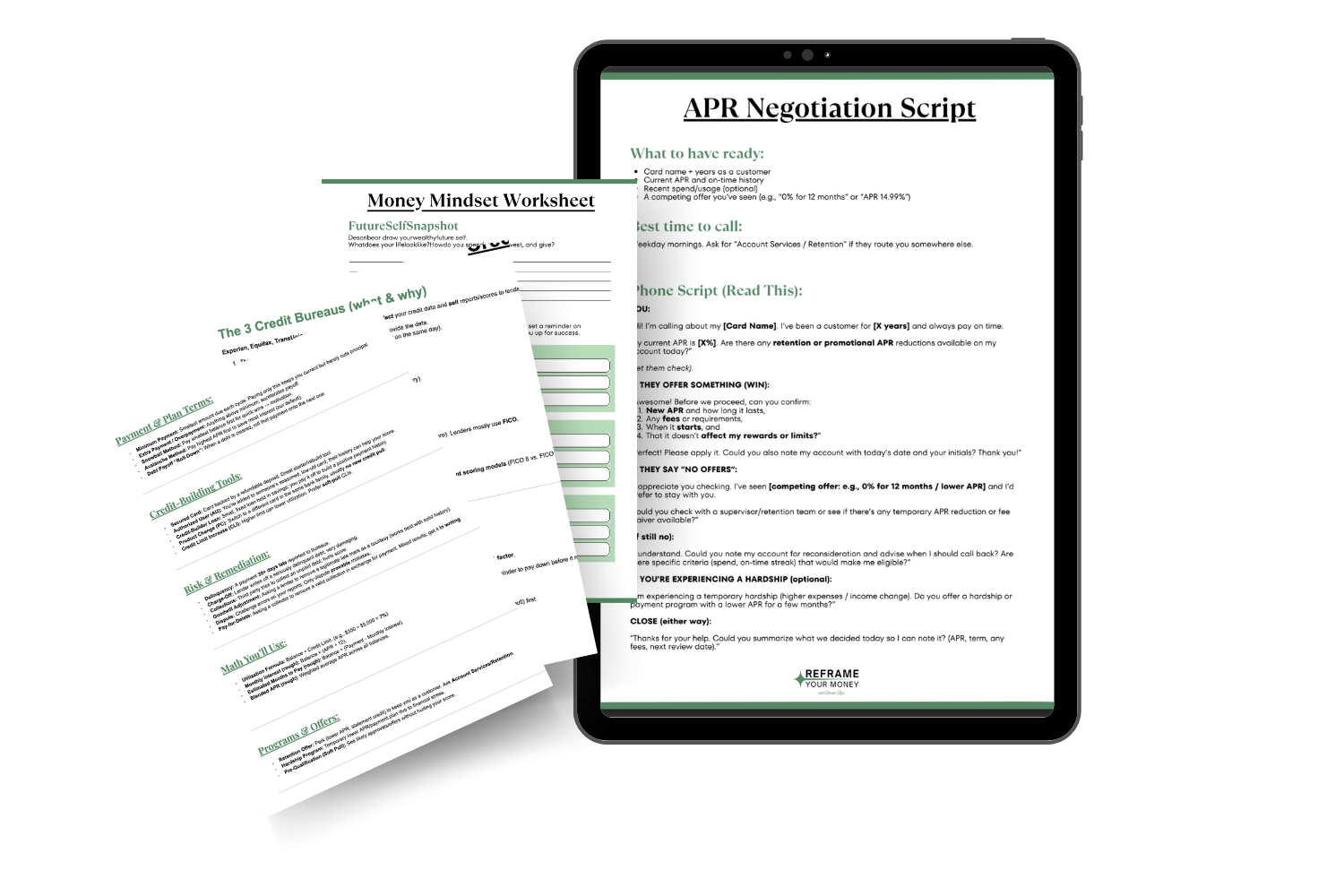

free bonus: 5 Done-for-you worksheets

free bonus:

5 Done-for-you worksheets

5 Done-for-You Worksheets:

- APR Negotiation Script:

The exact words to say when you call (no stumbling, no backing down)- Glossary of Financial Terms:

Decode the BS so debt can't confuse you anymore- FICO Score Breakdown:

Know what actually moves your credit score (and what doesn't matter)- Credit Bureau Contact Guide:

Direct contacts to dispute errors and fix what's broken- Debt Payoff Tracker:

Watch your debt disappear month by month

$19 Free*

5 Done-for-You Worksheets:

- APR Negotiation Script:

The exact words to say when you call (no stumbling, no backing down)- Glossary of Financial Terms:

Decode the BS so debt can't confuse you anymore- FICO Score Breakdown:

Know what actually moves your credit score (and what doesn't matter)- Credit Bureau Contact Guide:

Direct contacts to dispute errors and fix what's broken- Debt Payoff Tracker:

Watch your debt disappear month by month

$19 Free*

FAQ's

FAQ's

"Will this work if my credit is already trashed?"

YES. This is literally designed for the post-breakup mess. I filed bankruptcy, my credit was at rock bottom. If these strategies rebuilt my financial life from zero, they'll work for you.

"Do I need a bunch of extra money to make this work?"

Nope. You're going to use the money you're ALREADY paying toward debt, just in the right order this time. Plus, negotiating your APR alone could free up hundreds per month. That's your money coming back to YOU.

"What if I've tried to 'get out of debt' before and it didn't stick?"

Because you didn't have the breakup plan. You had motivation (which fades) and willpower (which runs out). This is about strategy and automation. You'll know exactly which debt to dump, when, and why. No guessing. No guilt.

"I'm not a spreadsheet person. Will I actually be able to use these tools?"

Absolutely. Every tool has a video walkthrough, and the scripts are copy-paste ready. If you can break up with someone via text (no judgment), you can use these tools.

"What if I feel guilty about 'giving up' on my debt?"

Let me reframe that: You're not giving up. You're getting OUT. Debt has been draining you, stressing you out, and keeping you small. This isn't about quitting, it's about finally choosing yourself. And that's not selfish. That's survival.

© 2025 Reframe Your Money

By visiting this page, you agree to Terms & Conditions

DISCLAIMER: This course is for educational purposes only and is not financial advice. I am not a licensed financial advisor, and the content provided is based on my personal experience and research. You should consult with a qualified financial professional before making any financial decisions. Individual results may vary based on personal circumstances, debt amounts, credit situations, and how strategies are implemented.

This site is not a part of the Facebook website or Facebook Inc. Additionally, This site is NOT endorsed by Facebook in any way. FACEBOOK is a trademark of FACEBOOK, Inc.

© 2025 Reframe Your Money

By visiting this page, you agree to Terms & Conditions

DISCLAIMER: This course is for educational purposes only and is not financial advice. I am not a licensed financial advisor, and the content provided is based on my personal experience and research. You should consult with a qualified financial professional before making any financial decisions. Individual results may vary based on personal circumstances, debt amounts, credit situations, and how strategies are implemented.

This site is not a part of the Facebook website or Facebook Inc. Additionally, This site is NOT endorsed by Facebook in any way. FACEBOOK is a trademark of FACEBOOK, Inc.